Turnabout on AGM

On September 28, 2021, Mary Ann San Juan, President & CEO of FCT, issued an Annual General Meeting (AGM) Letter postponing the AGM for October 2021 until further notice. Thus, 2021 would have been the second year of no AGM for its members. She stated Covid as the reason and that “a virtual meeting may not be a viable option for our members.”

Concerned members called out the following: firstly, why can FCT hold on September 19, 2021, an Appreciation Night for invited members, complete with formal dining tables and a buffet for about 60 guests but not a regular membership meeting, as required by its constitution?. Secondly, why can Community Centres Kalayaan and Markham Federation conduct their regular annual membership meetings despite Covid and use the virtual option for 2020 and 2021, while FCT cannot?

Fast forward three weeks later, on October 20, 2021, in a complete turnabout, Mary Ann rushed a Notice Letter (pictured), now scheduling an in-person AGM on November 14, 2021.

Where are the Financial Statements?

While it is always better to have an AGM, again as in the previous AGM’s, no Financial Statements are available ahead of time.

Article 6, Section F of the FCT Constitution provides that the “President and Chief Executive Officer shall present an annual report (financial and all other activities) at the annual general meeting and have it published in at least two Filipino community newspapers within a month of the general meeting.”

Its plain sense that members need time to review the statements before giving their approval, especially since for review are five years in a row – 2016, 2017, 2018, 2019 and 2020. But, more than that, unresolved financial questions are at the center of these years under Audit.

Credit to concerned members

The concerned members may have helped in finally nailing down an AGM this year. But definitely, more credit is due them for:

(1) Raising the financial and governance issues for proper governance and financial control

(2) Authoring the 2018 AGM motion for an Independent Third Party Audit, and

(3) For three long years – pressing the FCT Board to get the Audit done.

Third-Party Independent Audit

Sticking to the subject of the Independent Audit, in the May 2020 Open Letter to FCT Board of Directors (BOD), the concerned members stated:

“There are three reasons for the Third Party Independent Audit, namely:

- To assure the membership that FCT’s finance is in line with proper and standard accounting.

- To ensure that FCT’s operations are in compliance with its constitution and bylaws

- To confirm that FCT is operating with the spirit and guidelines governing a non-profit corporation.

To safeguard the independence and validity of a third-party audit, the following need to be in place:

- Membership is to be represented in the selection committee for the third party auditor.

- Membership is to be represented in defining the scope and requirements of the Audit.

- Membership is to be represented by the Third Party Independent Auditor of its audit findings and recommendations in a designated AGM or Special Membership meeting.”

FCT Board and Concerned Members collaborate

After repeated follow-ups, last March 21, 2021, the FCT Board finally relented and further ;consented to a membership representation in the independent Audit.

The FCT Board and the concerned members reached an agreement to form a Joint Task Group composed of five Board representatives, namely; Dr. Vicky Santiago, Dr. Nanette De Villa, Mary Ann San Juan, Theresa Lumanlan, and Wendy Arena and five concerned members, namely; Bay Bernabe, Corazon De Villa, Marilou Parcero, Luna Vince, and Noel Cruz.

On April 11, 2021, the Joint Task Group set up a Special Audit Committee (SAC) of four individuals – Theresa Lumanlan, Wendy Arena, Luna Vince, and Marilou Parcero. SAC subsequently established their Charter, Project Milestones, and Timetables. The Charter mandate prescribed the team as a temporary body that will be directly responsible for selecting an auditor and the oversight of the Auditor’s work who will provide audit services to the Filipino Centre Toronto. Included in the Charter were the structure, process, and accountability, and that SAC will be fully discharged of its responsibilities upon AGM approval of the External Audit Report.

SAC dutifully hammered out the Request For Proposal (RFP) document. In keeping with safeguarding the independence and validity of the Audit, the milestones section specified the review and presentation of the Auditor’s report to SAC, and then to the Joint Task Group and FCT Board for approval. The final presentation will be to the membership body at the October 2021 Annual General Meeting.

Concerned Members Audit participation short-lived

The SAC sessions were fruitful but were not without their difficult moments. On May 14, 2021, after finalizing the RFP, Luna Vince sent an internal personal email expressing her frustration at the time-consuming back and forth or flip-flopping. Inadvertently she copied in both Theresa Lumanlan and Mary Ann.

Instead of invoking the agreed conflict resolution as per SAC Charter to discuss and resolve the errant email, Mary Ann readily referred the matter to the Board, ignoring the conflict resolution process of the agreed Charter. Unfortunately, the Board, which dillydallied for three years on having an audit done much less in collaborating with the concerned members, wasted no time and arbitrarily so in disbanding both Joint Task Group and SAC, in total disregard of the notable progress in finalizing the Audit RFP, milestones and timetables.

Remedies to the problem, such as simply replacing Luna Vince with another concerned member, went unheeded. In the FCT Board’s minds, it could be that this was an opportunity to proceed with the Audit on its terms without the representation of the concerned members. It was sad that it took numerous emails and meetings to build the collaboration, yet just one email became a lame excuse to knock it down.

In the aftermath, the concerned members had asked that FCT share the Auditor’s scope and arrange an audience for the concerned members with the selected Auditor, but to no avail. The present Audit, therefore, has no participation or oversight whatsoever by the concerned members. Nevertheless, the hope is that the Audit is substantial and complete.

| Why does FCT BOD prefer to work with the Auditors behind closed doors? We wonder why? | |

| FCT BOD letter of Oct 25th item 2 states that “The independent auditor will perform the audit in accordance with the GAAP Accounting Standards. “ | We are confident that the Yale PGC LLP Auditors will definitely perform the audit to Canadian accounting standards within the limitation of the “statement of work” provided to them. Are we just as confident that the FCT BOD will provide the right type of audit statement of work? Readers, form your judgment. Concerned Members asked, emailed, texted numerous times to be involved in the scoping and selection process of Auditors. No answer. No response to the requests. We requested twice for a meeting with the Auditors in the presence of the BOD. Each request was met with a “ no response.” After all, the Independent Audit was a requirement of the AGM resolution of 2018 in response to rejected financial statements for 2016 and 2017 presented by then FCT accountant, Roman Chu. Members have the right to be part of the process. The Open Letter and Petitions of the Concerned Members from 2019 to 2021 specifically requested a joint collaboration effort in the audit engagement process. It is not known whether the Concerned Members’ 2 suggested Auditors were even given a fair chance to bid on the Audit Request for Proposal (RFP). We are sure Yale PGC LLP Accounting office did an outstanding job given the “scope” provided by the FCT BOD. Did the FCT BOD provide the following scope for a Compliance not Operation Audit ? One of the key proposed scope proposed by the Concerned Members was on Compliance Audit: To audit any significant or unusual transactions entered into such as the following:Cash Receipts and Disbursements,Accounts Receivables, Accounts Payables/Accruals,Reconciliation of Accounts, Leases and Contracts and Grants and Donations One of the FCT Officers insisted that Audit Engagements are the privilege of the BOD per the Constitution. That may be true under ordinary circumstances. However, on an extraordinary instance when an Independent Audit is approved as a motion due to rejected financial statements, it is the right duty of the BOD to involve designated members in the audit engagement and scope determination process.This is what respectable BOD members do. This is what respectable organizations do. This is how the BOD wins the confidence of its members. |

The Mystery of Financial Statements, AGM members approving “Draft Financial Statements”, and FCT President /CEO Skips a Financial Year ( 2016) to Review with AGM. Is this a new Hide and Seek Financial Reporting done by NPO BODs? Anyone knows of any other BOD that does this? | |

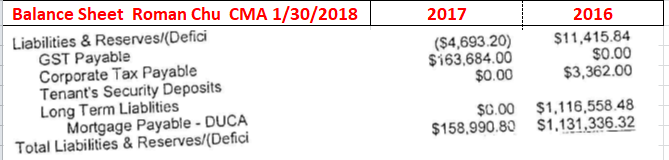

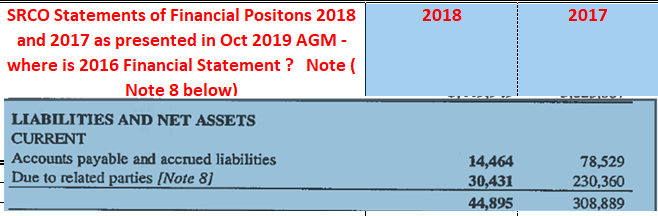

| FCT Letter item 3 states “ The Audited Financial Statements will be presented….” | We wonder what Financial Statements were provided to the Auditor to audit? The only proper Financial Statements to be given for audit are the 2019 AGM-rejected Statements for 2016 and 2017 prepared by Roman Chu in 2018. Note there are no Accounts Payable as of 2015 and 2016 as prepared by Mr Chu, the FCT Accountant at that time. Incidentally, FCT is no longer his client. There was no AGM in Oct 2017. FCT deemed as “ no quorum” after a phone survey prior to the planned AGM. Yes, folks, a volunteer-staffed phone survey deemed “ NO QUORUM.” Which Robert’s Law of Order does that follow? Anyone knows? In the Oct 2018 AGM, note there were no Accounts Payable as of 2017 and 2016 as presented by Mr. Chu. When members asked the accountant what happened to the $678,000 payables presented by the BOD in the Special General Meeting on Sept 2018. It was missing in the reported Payables and Paid.Mr. Chu was dumbfounded. He expressed surprise. Thus, the motion for the Independent Audit was raised, approved and resolved in Oct 2018 in a motion submitted by Bayani Bernabe.   In 2019, SRCO was hired by FCT BOD to do a Review Engagement of 2017 and 2018 Financial Statements . Note, although we are missing the 2016 Financial Statement, BOD did not give the 2016 FS to be reviewed to SRCO. Any opening balance used by SRCO for 2017 – was not approved by an AGM. This was what SRCO presented in Oct 2019 – DRAFTS Financial Statements (Draft written across all pages) – see photo.  So let us look at what SRCO’s Note 8 states:  Questions asked by members in that Oct 2019 AGM. Questions asked by members in that Oct 2019 AGM. 1. Where is the 2016 Financial Statement to approve ? Why hide? 2. What is the above Note 8 $548,296 about ?3. Where did the $678K payable disappear to? SRCO pointed us to ask “ Management” – the BOD. When we eventually asked the BOD, the FCT President and CEO simply avoided answering the questions and asked the AGM members instead to vote and approve the “Draft 2017 and 2018 Financial Statements ” with a 2016 Financial Statement as a no-show. FCT-nation of BOD members of 19 plus others approved the Financial Statements.Can one retain confidence on a BOD that presents DRAFTS for AGM vote? Can one retain confidence on a BOD that skips one year to vote on the following years? Note in a quorum of 30, there are already 19 BOD members. BIG QUESTION: FCT BOD then declares that they have switched accounting method from Cash to Accrual as of 2016. Questions : Did CRA provide a letter of approval in 2015 to switch accounting method as of 2016 reporting period? Or was the switch of accounting method requested by FCT in 2019 to have next reporting period switched to Accrual only as of 2020 Financial Statements?Can this CRA approval letter be provided in the Nov 14, 2021 AGM? Per CRA site on Accounting Method: https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/sole-proprietorships-partnerships/accounting-methods.htmlIt says that a permission letter must be obtained from CRA to switch accounting method as of the following year, not retroactively.  |

Payments to certain Board Members

Article VII, Section 4 – Remuneration and reimbursement, clearly states that:

“Members and officers of the Board of Directors, officers of the Executive Council and members of the Filipino-Canadian Centre shall receive no remuneration from the organization acting as such. They shall be reimbursed of reasonable expense(s) incurred in the performance of duties”.

After the sale of the building for $5.9 M, FCT Board has been seeking refuge under Board resolutions to justify payment of salaries to co-directors and certain FCT members. It is questionable that a board resolution is sufficient to authorize payment to directors/members, much less retroactive salary payments for over ten years. An amendment by 2/3 of the members to Article VII, Section 4 is necessary to authorize salary payments, as per Section 1 of the Corporations Act.

To refresh the Board’s memory, tabled in their published Agenda for the Annual General Meeting of November 26, 2017, were the following items for consideration and approval of the membership:

Agenda Item # 4

Amendments to the FCT Constitution and By-laws: (i) reducing the quorum requirement for meetings from a majority of members; and (ii) providing for authority to remunerate persons who are directors and officers of the Corporation for the provision of services to the Corporation in another capacity.

Agenda Item #5

Authorizing the payment of: (i) remuneration to certain directors and /or officers for past services provided to the Corporation in a capacity other than as a director and/or officer; and (ii) reimbursement of expenses incurred by certain persons arising from them having acted as directors and/or officers of the Corporation in relation to certain legal proceedings which they were part of and generally fulfillment of any indemnity that they may have.

Agenda Item #6

Confirmation of all past acts and things undertaken/conducted by the Board of Directors and/or members (including but not limited to) waivers of notices or technical irregularities that may have arisen with respect to notice of and/or the conduct of meetings.

The Board must have had legal advice to do what is legitimate and correct. On November 26, 2017, the attempt was there to secure the bylaw amendment, but the Board cancelled the meeting allegedly due to lack of quorum. That was the last time the membership would ever hear of a bylaw amendment. The Board apparently abandoned the amendment option and has opted to go the fast, easy, though highly questionable way of just passing resolutions.

The Board offered no reason whatsoever in subsequent AGMs for this change of heart. Is it because FCT has already paid over $400,000 in salaries either in part or in whole? Even in the ‘well-controlled and no press allowed’ Special General Meeting of June 2019, FCT offered nothing but the usual Board resolutions as the answer. It appears a Board resolution is a key and remedy for FCT in address financial concerns, particularly on payables.

Membership misled

FCT states in its most recent press release that:

“The FCT as a not-for-profit, volunteer run, and community service organization is determined and has been reasonably operating to meet its mission and mandate with full trust and support by its directors, officers, and members.”

Most community members view volunteerism as a non-salaried service. And if it is paying salaries or regular monthly gas allowance of $1,250, then surely the members ought to know during AGMs, all Board directors ought to be aware, and the financial statements year to year ought to report such wages. However, to keep it from the members, from other Board members, and any reporting in the financial statements from the very beginning, and only disclose them only after generating an income of $5.9M from the sale of the Parliament building, and only after the submission of $678,000 worth of payables makes for total mistrust and terrible optics.

Transparency is sorely missing in the FCT Board’s press statement above. As a result, full trust and support for the Board can only be shaky at best.

Accountability for legal bills

Continuing on transparency, the Board disclosed during the September 7, 2017, AGM that legal bills of $300,000 need to be settled. However, in the previous 2016 AGM, the Board told the members that only $30,000 legal bills were outstanding.

FCT as an organization may be accountable for legal bills. At the same time, FCT directors as plaintiffs in a court case may be responsible personally for their legal bills, not FCT. Members have been asking for a breakdown of the $300,000. Up till now, none has been made available. Did FCT pass another resolution to take care of personal legal bills of officers and directors?

Problem in perspective. The audit is not the end-all.

FCT leadership faces a mixed bag of serious issues. It all started with simple reimbursements after it liquidated its prime asset for $5.9 M.

Problems mushroomed when the membership found out that claims for reimbursement ran into hundreds and thousands of dollars. Then more revelations trickled in, such as the claims were found to be retroactive for salaries and allowances more than ten years back. Together with this is the discovery that the yearly financial statements did not record these claims. Furthermore, during all the Annual General Meetings, no mention was made to the members of these monthly salaries and gas allowances. Members thought the services rendered were a labour of love and voluntary. The constitution said so. It was, however, too late the dam had already burst.

So now it is evident the mixed bag contains financial, communications, governance, control, reporting, process, and transparency issues. All these affect the trust in the FCT leadership and the confidence and support of its members.

The damage control, correction, and recovery should happen. Resolutions don’t exactly help, but admissions, corrections, and improvements do. The failed collaborative effort on the audit between the concerned members and the Board was a lost opportunity.

Let us keep in mind the Independent Financial Audit is only a start. It is not the end-all. Many questions not necessarily addressed by the financial audit remain. Members hope to see what the audit findings and recommendations will be. To repeat the audit would be all dependent on the terms of reference and scope followed.

We shall see.